The Long Arc of Crypto

Investing in crypto is an exercise in perseverance. Both long-term and short-term investors in the space have faced wild volatility for more than 15 years, whipsawed between the excitement of new innovations and the pain of macro, regulatory and self-inflicted setbacks. Over the course of the 17 years since the introduction of the Bitcoin whitepaper, however, when you pull up to 35,000 feet and look down, you see the inexorable march of forward progress.

We can see this both through the lens of technical progress and real-world adoption, and also in the growth of the total market capitalization of the entire space.

Investment Progress

Long-term investors who have stuck with crypto through its bull and bear markets, its dark and bright times, its progress and setbacks, have been rewarded with somewhat unrivaled investment gains. Bitcoin remains the best-performing investable asset class in 11 of the past 14 years and the best cumulative performer over that time. This is true despite eras of opposition that alleged that “Bitcoin is just for piracy”, “Blockchain not bitcoin” and even Jamie Dimon’s House testimony in 2022 denigrating crypto to be just “decentralized Ponzi schemes”. Bitcoin, and crypto more broadly, has been a non-consensus investment sector for most of its history. We believe that era has now ended. While much still remains to be built and adopted, we contend that we are now past a period of uncertainty about long-term adoption and the value of crypto.

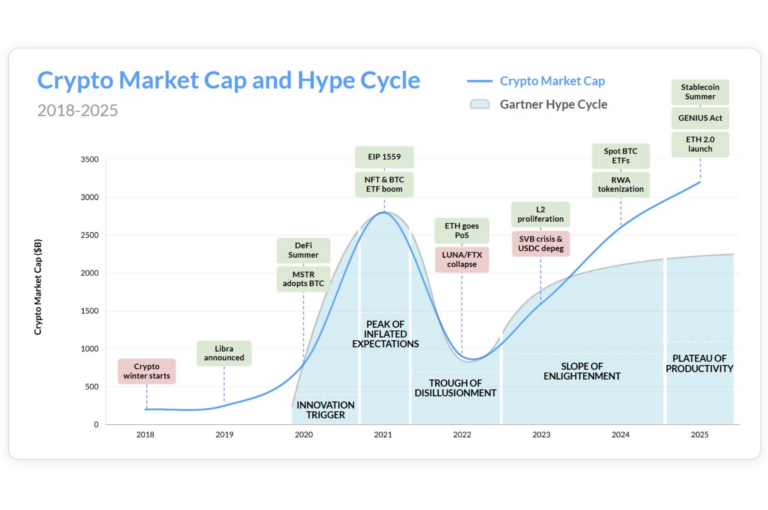

Below we can see the major positive and negative events in the crypto ecosystem and the corresponding total crypto market cap ($3.8 trillion as of this writing) over time. Despite the volatility, cynicism and doubt, tens of thousands of global software developers focused on building decentralized, permissionless networks suitable for many use cases and created an entirely new industry worth almost $4 trillion.

Fundamental Progress

For those of us closely following developments in crypto, these highlighted inflection points stand out as major de-risking moments despite the distractions of market noise and negative sentiment from the mainstream press, tech and finance sectors:

Among the many examples above of important inflection points in the historical record, we believe addressing Ethereum’s scalability issues through the proliferation of layer-2 blockchains is notable. The market appreciated these scalability solutions early on, as these networks managed to earn multi-billion dollar valuations despite launching their tokens soon after the black swans of Luna and FTX. These networks demonstrated originality in their technical approach (in both optimistic- and zero-knowledge-based rollups for example). At the same time, they were able to successfully compete for developer and investor mindshare and rise above the market noise, and also enable derivative solutions (cross-chain messaging, bridges and related aggregation), seeding new business models and further aligning with the inherent free market ideas of cryptocurrency technologies. For those of us focused on the future of blockchains, this felt like a major de-risking moment that has led to the market successes today.

Predicting Adoption Cycles

In tech, three main mental models primarily are used to help predict the path or cycles of tech adoption:

- The Gartner Hype Cycle

- Carlota Perez’s “Technological Revolutions and Financial Capital”

- Geoffrey Moore’s “Crossing The Chasm”

If you overlay the recent years of the total crypto market cap chart with the well-understood Gartner hype cycle (see chart below), the Carlota Perez four cycles of technological revolution, or the Geoffrey Moore “Crossing The Chasm” graph, you see that we are through the higher risk and overly exuberant phases of the tech buildout of decentralized systems and are now into the deployment period, or the slope of enlightenment or the early majority adoption phase.

What are the use cases of crypto networks being adopted now? First and foremost, the use of blockchains as payment rails for stablecoins. We have discussed this topic many times, and the total number of senders of stablecoin payments on just Ethereum recently passed one million in a week for the first time. The slope of the graph below supports our view that we are over the adoption hump here.

As The Block states, “From January 2020 to July 2024, there was an average of ~400,000 stablecoin senders on Ethereum per week. Since August 2024, this figure has grown by over 1.7% per week on average, consistently setting record highs. In 2025, there were, on average, 720,000 unique senders on Ethereum per week, while in the past two weeks alone, this number has surpassed one million weekly unique stablecoin senders.”

Flowing directly from the benefits of stablecoins, we see exploding usage in onchain wagering, gaming, prediction markets and other real-money entertainment and risk-taking. Per Artemis data, September 2025 saw $3.3T of transaction volume, adjusted to exclude MEV and intra-exchange volumes, an all-time high.

More specifically, we see the more recent acceleration of fundamental and investment activity on prediction markets as a multi-year, not overnight, success that is only possible onchain. While Augur (an early CoinFund investment) was launched in 2018 after originally being crowdfunded in 2015 and was too early to be very successful, the more recent volumes seen on Polymarket validate the idea that blockchain-based rails are the most fair, accessible, and auditable instantiation of the efficient market hypothesis as applied to event prediction, with Polymarket’s accuracy relative to real world outcomes continuing to improve. We have also been active on this front and have made several unannounced investments in adjacent opportunities with meaningful outcome potential.

We see similar excitement, albeit at an earlier stage, in our companies focused on decentralized AI. Decentralized training, GPU marketplaces and decentralized data and model solutions are experiencing strong interest in terms of investor follow-on appetite, while also progressing with public awareness and early network adoption.

In the past three years, significant amounts of regulatory, technological and adoption risk have been removed from crypto, yet we have not yet seen a step-function increase in the amount of venture capital invested in the early stages. Given the summary above of the existence and early adoption of the major building blocks required for crypto’s long-term success, we now firmly believe that crypto has moved from a non-consensus category to the early stages of consensus-driven adoption and integration. It will remain a dynamic and volatile investment category. For those of us carefully analyzing the shortcoming and missing pieces over the years, and then tracking the emergence of solutions and adoption data, we believe we have witnessed the zero to one moment giving us confidence in crypto’s staying power.

***

Disclaimer: The views expressed here are those of the individual CoinFund Management LLC (“CoinFund”) personnel quoted and are not the views of CoinFund or its affiliates. Certain information contained herein has been obtained from third-party sources, which may include portfolio companies of funds managed by CoinFund. While taken from sources believed to be reliable, CoinFund has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by CoinFund. An offer to invest in a CoinFund fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by CoinFund, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by CoinFund (excluding investments for which the issuer has not provided permission for CoinFund to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://www.coinfund.io/portfolio.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. This presentation contains “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially and adversely from those reflected or contemplated in the forward-looking statements.

David Pakman is a Managing Partner and Head of Venture Investments at CoinFund, focused on leading the firm’s venture investing activities. David developed an early interest in mining Bitcoin before he began building Ethereum mining rigs in 2017.

David is widely recognized for his track record and thought leadership in crypto, consumer, and enterprise technology investing. During his 13 years at Venrock he led the Series A round and sits on the board of Dapper Labs, led the Series A and B rounds of Dollar Shave Club (sold to Unilever for $1B), and led early-stage investments in robotics, AI, consumer and carbon removal tech companies. He personally invested in Coinbase prior to their IPO and was named the 55th top venture capitalist in the world by CB Insights.

Prior to CoinFund, David was a partner at venture capital firm Venrock, co-founder of Myplay, CEO of eMusic and the co-founder of Apple’s Music Group. David is a graduate and a former member of the Board of Overseers at the University of Pennsylvania’s School of Engineering and Applied Science with a degree in Computer Science Engineering.