The New Era for Business Banking and Payments: Investing in Dakota

With contributions from Einar Braathen & George Christopher

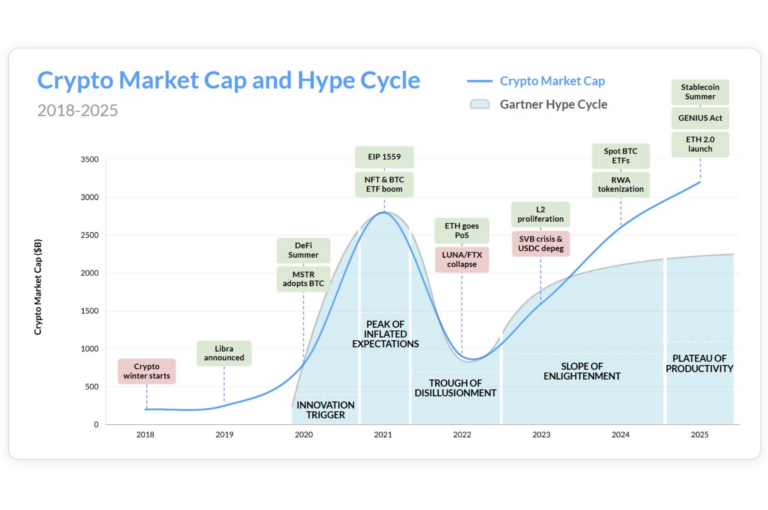

It’s Stablecoin Summer, and the adoption of stablecoins marks a profound shift in how value moves across the internet. Stablecoins are programmable, borderless, and instantly transferable. They represent the first real implementation of internet-native money, which is cheaper and faster than fiat moving on traditional rails and is poised to disrupt the massive global payments industry.

Thinking about it as an API for money, tokenized assets can be easily integrated with software. In 2023, there were 3.4 trillion transactions globally, which moved $1.8 quadrillion in value and generated revenue of $2.4 trillion. By 2024 the total volume of stablecoin transactions on public blockchains exceeded the combined annual volume of Visa and Mastercard at $28 trillion. Notably this activity precedes the GENIUS Act being passed by the House and signed into law, which will mark a pivotal step toward regulatory clarity, signaling bipartisan recognition that internet-native dollars are becoming foundational to the future of global payments. This is not the future — it is already happening. And yet, the financial tooling available to businesses is immature.

A key part of our payments thesis is the idea that whoever controls the transmission of money, controls the world. Today’s traditional money movement workflows rely on a patchwork of bank accounts, FX intermediaries, entity-specific compliance tools, and manual reconciliation processes. In the legacy system, accounts are internal ledgers managed by each financial institution, settlement requires reconciliation between books, and trust is established through intermediaries — banks, clearinghouses, and correspondent institutions — each adding cost and latency. This architecture made sense in an era of paper-based systems and limited connectivity. But it has reached its limits. Most businesses still route through multiple intermediaries to make a cross-border payment. A stablecoin needs none.

While neobanks are typically constrained to a single banking partner and serve as a wrapper on top of legacy systems, in an ideal world you would begin with the assumption that crypto rails are critical components of the future financial stack. This paradigm shift offers the opportunity to reshape simple fintech interfaces from a regional focus to global coordinators. A platform like this allows businesses to orchestrate payments, manage fiat and crypto tokens seamlessly alongside one another in their treasury, and administer global entities through a single, programmable interface. For businesses operating across borders and using multiple currencies, this can unlock a significant reduction in operational cost and complexity.

This is why we led Dakota’s $12.5 million Series A funding round, as the team is building the valuable layer that enables businesses to operate fluidly across both fiat and crypto-native rails. Led by Ryan Bozarth and Gabe G’Sell, the team has product in their DNA, with previous experience at Coinbase, Anchorage, Square, and Airbnb. Ryan has deep expertise in building secure and scalable crypto financial products. He is the former CEO of Coinbase Custody where he scaled its institutional custody platform to secure over $100B in assets and prior to that was head of product at Anchorage. Gabe G’sell is the former founder of multiple tech ventures. One venture, Deco, an IDE platform was acquired by Airbnb. Their goal is to utilize the efficiency of crypto rails, while meeting customers where they are. One of their core beliefs is that users shouldn’t have to be infrastructure specialists. Dakota is building a modern financial stack for businesses that simplifies stablecoin payments and onchain transfers. The platform already has over 500 customers and has processed billions of dollars in transaction volume to date.

Dakota has built for real world needs, and the team recognizes that every modern business will, eventually, need to interact with crypto rails, whether to accept stablecoins from customers in emerging markets, pay vendors instantly across borders, or manage treasury in programmable, real-time ways.

They collapse much of the old financial rails into software, building a platform that integrates blockchains, stablecoins, traditional banking rails, compliance policies, and accounting logic. As Ryan notes: customers are switching to Dakota because traditional banks are not built for today’s global economy. Crypto infrastructure upgrades the engine under the hood, because in a wallet-centric system, the ledger is shared and globally accessible. A wallet is not an account; it is a pointer to funds you can control. Record-keeping, finality, and auditability are no longer outsourced to banks—they are built into the system itself.

At the same time, Dakota’s founders are aware that adoption requires more than access, it requires abstraction. The system must be easy to use, compliant with regulation, and interoperable with traditional tools. Modernizing the transfer of value means plugging in banks into the platform as nodes and refocusing on their role as endpoints in the real world, instead of intermediaries. By orchestrating bank accounts, wallets, and third-party financial APIs like Circle, Stripe, and local payment processors, Dakota gives businesses a single place to manage funds.

The initial target customers for Dakota include cryptonative enterprises, companies hiring or selling internationally (typically found in the SaaS and marketplace verticals), global services firms and non-profits. As more and more companies participating in the global economy recognize the benefits of crypto and stablecoin based payments, we expect the target customer base to continue to expand. We believe that this increased recognition, alongside improved regulatory clarity, will be a strong tailwind for Dakota’s growth and the sector’s advancement as a whole.

Our conviction in Dakota rests on a seasoned founding team, a product primed to revolutionize the large global payments market, and regulatory catalysts. In the past month since the successful Circle IPO, we’ve heard it called “crypto’s chatGPT moment.” Existing vertical banking startups, be it sector-specific or geography-specific banks, are often built atop traditional infrastructure and optimize around existing constraints. We believe that Dakota is different. It is not defined by a geography, a sector, or a regulatory arbitrage. It is defined by an architecture: global, programmable, and modular. In our view, this is the correct orientation. And the good news for the crypto sector at large is that as a massive amount of value moves onchain via stablecoins and other tokenized assets, we think people will look downstream for things to do with it within the crypto ecosystem.

We’re proud to support the team in bringing onchain finance to all enterprises.

***

Disclaimer: The views expressed here are those of the individual CoinFund Management LLC (“CoinFund”) personnel quoted and are not the views of CoinFund or its affiliates. Certain information contained herein has been obtained from third-party sources, which may include portfolio companies of funds managed by CoinFund. While taken from sources believed to be reliable, CoinFund has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by CoinFund. An offer to invest in a CoinFund fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by CoinFund, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by CoinFund (excluding investments for which the issuer has not provided permission for CoinFund to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://www.coinfund.io/portfolio.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. This presentation contains “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially and adversely from those reflected or contemplated in the forward-looking statements.

Alex Felix is CIO and Co-Founder at CoinFund, leading investments in companies and protocols from pre-seed to Series A. As a former world-class ski racer, Alex has since focused his ambitions on becoming a leading web3 investor driven by a passion for fintech and crypto. Discerning and prescient, he has personally and professionally invested early in over 100 blockchain-focused companies since 2013, spanning many widely recognized names including seed rounds of Ethereum and Blockdaemon.

Prior to CoinFund, Alex spent 10 years across research, investing and structuring. Most recently, he arranged buyouts for American Capital, a private equity firm based in New York. Alex also held roles at BofA Merrill Lynch, RBS and Guggenheim Partners. He is an active technology angel investor and has built ecommerce algorithms. Alex has a degree in Economics and Earth Sciences from Dartmouth College.